How Do I Get Out of a Timeshare Loan?

You can get out of a timeshare loan by exercising your legal right to rescind (if still within the cancellation window), contacting the developer directly, or hiring a reputable timeshare exit company that provides attorney-based solutions to negotiate your release.

Timeshares: Sold as a Dream, Delivered as Debt

Let me guess—you were on vacation, enjoying yourself, when a sales rep offered you a free breakfast or show tickets if you attended a short presentation. Hours later, you were signing a contract for a timeshare. Sound familiar?

They sell it as an affordable way to make family memories. But here’s the truth—timeshares are not investments. They’re liabilities. Financial advisors warn people not to touch them with a ten-foot pole. They lose nearly all value the second you sign the dotted line.

A couple from Ohio who contacted our company that had just bought a $25,000 timeshare on a 10-year loan the previous year. They ended up paying almost $8,000 in the first year of owning. This was more than they spent for their actual family vacations over the past several years – and they haven’t even booked a vacation yet with the timeshare due to limited availability. When they looked into reselling it, they realized they couldn’t even give it away.

The True Cost of a Timeshare Loan

Most timeshare loans are set up for 120 months at sky-high interest rates—often 15% or higher. And they’re front-loaded, which means for the first 5 years, you’re mostly paying interest, not principal. If you’re thinking about taking your sales rep’s advice on refinancing the high interest with your bank—don’t waste your time. Banks will not refinance a timeshare loan and the last thing you want to do is take a loan out against your home to pay off the high interest timeshare loan.

Cost Breakdown of a Timeshare Loan (2025)

| Loan Feature | Typical Value | Financial Impact |

|---|---|---|

| Loan Length | 120 Months | Long-term commitment |

| Interest Rate | 15%–18% | High monthly interest |

| Down Payment | $5,000+ via credit card | Creates secondary debt with interest |

| Year 1–5 Payments | 70% to interest | Little reduction in loan principal |

| Annual Maintenance Fee | $1,200–$1,800 | Increases over time, not optional |

The Credit Card Trap

Here’s another dirty trick: many timeshare sales teams will put your down payment—usually $5,000 or more—on a branded credit card. We’ve seen this with cards from Barclays, Comenity Bank, American Express, and others. They’ll even set up your loan autopay to charge the same card. So now you’re paying double-digit interest on both the loan and the card. If you’re only making minimum payments, you’re getting buried in debt.

Why You Must Get Out of a Timeshare Loan Now

You’re paying through the nose for something you probably don’t use as often as they claimed you would. Add to that the annual maintenance fees that keep going up, and you’re stuck with a financial black hole.

And if you’re wondering, “How can you get out of a timeshare loan without destroying your credit?”—you’ve got limited options and will need to act fast.

Legal and Practical Ways to Exit Timeshare Loan

1. Cancel During the Rescission Period

Every state has a law that gives you a window—usually 3 to 10 days—to cancel your timeshare after purchase. You must do it in writing. Check your contract for the details.

2. Contact the Developer

If you’re past that window, contact the timeshare developer. Some have formal exit programs, but be warned—they often just offer to resell it for you (which rarely works) or reduce your payments in exchange for extending the loan.

3. Bring a Legal Claim

If you were misled or experienced false advertisement, you might have grounds for legal action. An experienced attorney can review your timeshare complaint and identify violations or false claims.

4. Hire a Legitimate Timeshare Exit Service

Look—this is where most people go wrong. There are a ton of scammy timeshare exit companies out there. But there are also legitimate firms that use attorney-based solutions to help you cancel the contract and walk away legally and permanently.

Here’s what to look for:

- Over 10 years of experience

- Legal support with licensed attorneys

- Positive reviews and Better Business Bureau accreditation

We once helped a couple that were financially burdened by a timeshare they owned out of Colorado. They were $200k deep in a timeshare mess. With assistance from our attorney-based service, they exited the contract and were debt-free in under 12 months.

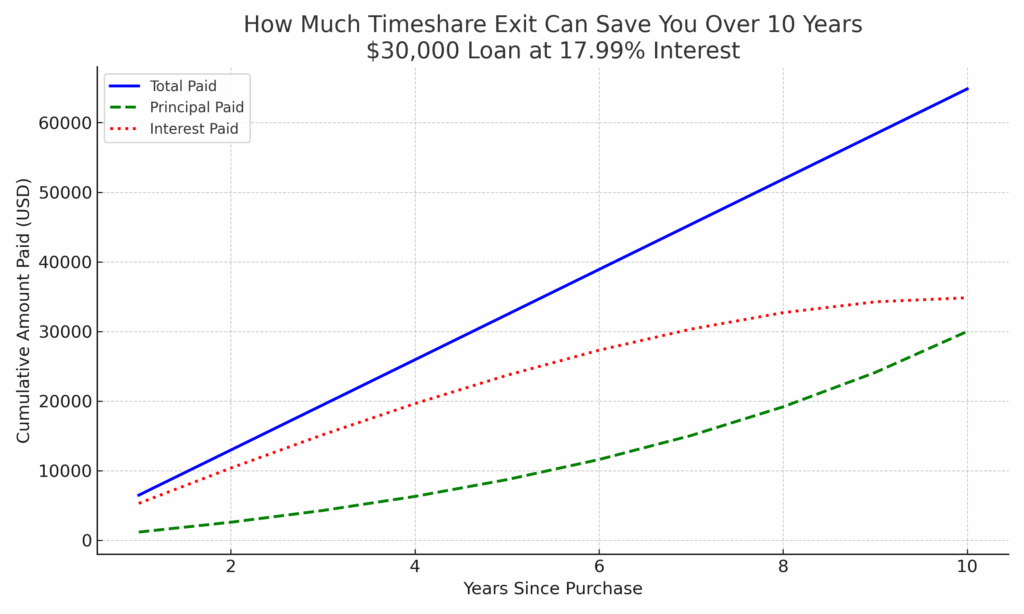

How Much Timeshare Exit Can Save You Over 10 Years

Let’s put it in perspective: On a $30,000 loan at 17.99% interest, you’ll pay over $64,000 over 10 years when you include interest and principal. This is not taking the mandatory maintenance fees into consideration, which can easily run you another $10,000 over this period of time. Exiting now can save you tens of thousands of dollars for your family.

Final Word: You're Not Alone, and You're Not Stuck

You didn’t make a dumb decision—you were targeted by trained salespeople. We know how you got roped into this, and we’ve helped thousands of families walk away from these one-sided contracts.

If you’re asking, “How do I get out of a timeshare loan?” the answer is: you can—and you should.

We offer no-cost consultations to understand your story and how we may be able to assist in your timeshare exit journey.

Contact us today. Get your peace of mind—and your financial freedom—back.